Project cost management helps deliver a project within the approved budget. It includes planning, estimating, budgeting, and controlling costs. Project managers must define their projects well. They must also give realistic time and cost estimates.

Cost is measured in money, like dollars or rupees. Managing cost is critical for a project’s success. Poor cost control can lead to failure.

Table of contents

- What Is Project Cost Management?

- Key Components of Project Cost Management

- Basic Principles of Cost Management

- Role of the Project Manager

- Profits and Financial Terms

- Real-World Example: Seminar Project

- Case Study: Practical Cost Management

- Project Life Cycle and Cost Management

- Core Objectives of Project Cost Management

- Key Processes in Project Cost Management

- Final Words

- Related Articles

What Is Project Cost Management?

Project cost management ensures a project finishes within its approved budget. It involves planning, estimating, budgeting, and controlling costs. These steps help deliver value while managing limited resources. The goal is to meet project goals without overspending.

Cost management is a part of the triple constraint. This includes scope, time, and cost. All three must balance for a successful project. If one changes, others will also shift.

Project managers must track costs from start to end. They must plan and manage funds throughout the project life cycle. This prevents delays, overspending, and poor decisions.

Public, Onsite, Virtual, and Online Six Sigma Certification Training!

- We are accredited by the IASSC.

- Live Public Training at 52 Sites.

- Live Virtual Training.

- Onsite Training (at your organization).

- Interactive Online (self-paced) training,

Why Is Project Cost Management Important?

Every project requires money to buy resources. This includes people, equipment, and materials. Cost management ensures those expenses are tracked and controlled.

It helps teams work within financial limits. It also prevents waste. When done right, it boosts profits and builds trust with stakeholders.

If you don’t manage costs, projects can fail. You might run out of money before reaching goals. That leads to delays or unfinished work.

Without proper cost management, even well-executed projects may fail due to overspending. Stakeholders, especially executives and investors, care deeply about whether a project stays within budget and provides a return on investment.

Key benefits include:

- Better financial control

- Improved decision-making

- Reduced risks of overruns

- Enhanced stakeholder confidence

- Increased profitability

Main Goals of Cost Management

- Keep the project within budget.

- Use resources efficiently.

- Track spending and adjust when needed.

- Provide accurate cost reports to stakeholders.

- Support decision-making using financial data.

When Does Cost Management Start?

Cost management starts during the planning phase. It does not begin after approval. Planning early avoids costly surprises later.

Cost decisions affect project design, resources, and scheduling. If you skip early planning, you may face budget problems later.

Also Read: Project Portfolio Management

Key Components of Project Cost Management

Project cost management includes four main processes:

- Plan Cost Management

- Estimate Costs

- Determine Budget

- Control Costs

Each process plays a specific role. Let’s break down each one.

1. Plan Cost Management

This is the first cost process. It creates a plan for managing project costs. It defines how to estimate, budget, and control spending.

The plan includes:

- Rules for cost control

- Cost measuring units

- Roles and responsibilities

- Reporting formats

It acts as a guide for the entire project. It also helps stakeholders understand how costs are tracked.

2. Estimate Costs

In this step, teams estimate how much resources will cost. This includes labor, equipment, materials, and services.

Estimating helps answer: How much will this project cost?

Types of estimates include:

- Rough Order of Magnitude (ROM): Early guess, low accuracy

- Definitive Estimate: More accurate, done later in planning

Estimates can be:

- Analogous: Based on past similar projects

- Parametric: Uses data and formulas

- Bottom-up: Detailed and specific

- Three-point: Uses optimistic, pessimistic, and most-likely values

All estimates should include potential risks and reserves.

3. Determine Budget

This process combines all cost estimates into a total budget. It assigns costs to each project activity or work package.

The result is a cost baseline. This is a reference point for measuring cost performance.

Budgets include:

- Direct costs: Linked to specific activities (e.g., labor)

- Indirect costs: Shared across activities (e.g., admin costs)

- Contingency reserves: For known risks

- Management reserves: For unknown risks

The budget must match the project funding limits.

4. Control Costs

Cost control tracks spending and compares it to the budget. It helps detect cost overruns early.

This process answers:

- Are we on budget?

- If not, why?

- What can we do about it?

Control tools include:

- Earned Value Management (EVM): Tracks cost and schedule

- Cost variance (CV): Shows if you’re under or over budget

- Trend analysis: Predicts future performance

Teams must act quickly if costs deviate. Delays in response can worsen problems.

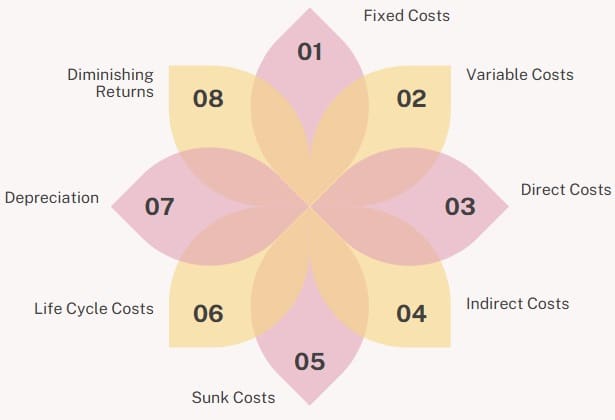

Basic Principles of Cost Management

Here are some essential cost concepts:

1. Fixed Costs

These stay the same, regardless of work done. Example: office rent.

2. Variable Costs

These change with work output. Example: hourly wages or materials.

3. Direct Costs

These relate to specific tasks. Example: contractor fees.

4. Indirect Costs

These are shared across tasks. Example: utility bills.

5. Sunk Costs

These are already spent and unrecoverable. They should not affect new decisions.

6. Life Cycle Costs

This includes total cost from project start to product retirement. It covers development, use, support, and disposal.

7. Depreciation

Depreciation is loss of value over time. Two types are:

- Straight-line: Equal value lost each year

- Accelerated: Higher loss early on

8. Diminishing Returns

The more you invest in something, the less benefit you get per input.

Also Read: Project Risk Management

Cost Management Tools and Techniques

Project managers use several tools to manage costs:

- Expert Judgment: Knowledge from past projects

- Cost Estimating Software: Helps create detailed estimates

- Spreadsheets: Useful for simple tracking

- Project Management Software: Integrates cost, scope, and schedule data

- Meetings: Align teams on budget and changes

Common Cost Management Challenges

Cost management isn’t easy. Here are a few common problems:

- Underestimating project costs

- Scope changes increasing costs

- Unexpected expenses

- Poor communication about budgets

- Lack of cost control systems

Project teams must update plans as the project evolves. Flexibility is key to managing surprises.

Importance of Stakeholder Satisfaction

A successful project delivers value to stakeholders. Cost control helps meet expectations. Stakeholders care about:

- On-time delivery

- Quality results

- Staying within budget

If you control costs well, trust increases. This improves project outcomes.

Also Read: What is Project Scope?

Role of the Project Manager

The project manager owns the cost management process. They must:

- Create a realistic budget

- Track expenses

- Report cost performance

- Adjust plans when needed

- Communicate clearly with the team and stakeholders

They must also understand financial terms. This helps when speaking with executives.

Profits and Financial Terms

Executives care about profits. Profit is revenue minus cost. A profit margin is the percentage of profit from revenue.

Example:

- Revenue: $100

- Profit: $2

- Profit Margin: 2%

If costs rise, profit drops. This is why cost control matters.

Real-World Example: Seminar Project

Imagine planning a seminar. Here’s how cost types apply:

- Fixed cost: Room rent

- Variable cost: Meals for attendees

- Direct cost: Renting a sound system

- Indirect cost: Electricity shared with other events

This example shows how different cost types interact.

Case Study: Practical Cost Management

In real projects, teams:

- Estimate costs using past data

- Budget based on labor, services, and equipment

- Control costs using regular reporting

They compare actuals to the baseline. This helps them act fast when problems arise.

Project Life Cycle and Cost Management

Cost management is part of each phase:

- Initiation: Early estimates

- Planning: Detailed budgets

- Execution: Cost tracking

- Closure: Final reporting and lessons learned

Cost management does not stop when the project ends. Lessons learned help future projects succeed.

Core Objectives of Project Cost Management

Keeping expenditures within the approved budget: This is the primary goal, preventing cost overruns and ensuring financial viability.

- Making informed decisions: Providing accurate cost data to help project managers make strategic decisions about resource allocation, risk management, and scope adjustments.

- Improving efficiency and profitability: By carefully tracking and controlling costs, projects can be delivered more cost-effectively, leading to better financial outcomes for the organization.

- Aiding future planning: Historical cost data from managed projects can be used to improve the accuracy of estimates and budgets for future projects.

Project Cost Management is a crucial aspect of project management that involves the processes required to plan, estimate, budget, and control costs throughout the project lifecycle to ensure the project is completed within the approved budget. It’s about making sure that the financial resources are used efficiently and effectively to achieve project objectives.

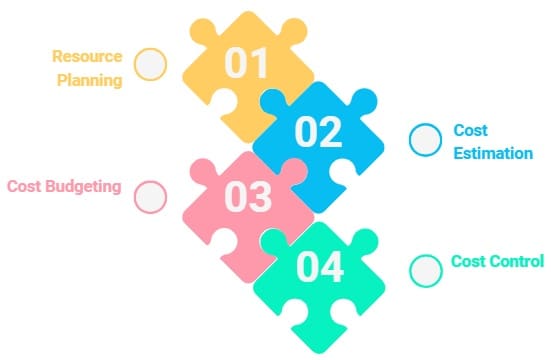

Key Processes in Project Cost Management

While often viewed as a continuous process, project cost management typically involves four main, often sequential, steps:

- Resource Planning:

- This initial step involves identifying all the resources (people, equipment, materials, technology) required to complete the project activities.

- It often starts with a Work Breakdown Structure (WBS) to break down the project into smaller, manageable tasks, and then determining the resources needed for each task.

- Cost Estimation:

- Once resources are identified, this step focuses on approximating the monetary cost of all those resources for each project activity.

- Various techniques can be used, such as:

- Analogous Estimating: Using actual costs from similar past projects.

- Parametric Estimating: Using mathematical models based on historical data and project parameters.

- Bottom-Up Estimating: Estimating costs for individual work packages and then summing them up.

- Three-Point Estimating: Considering optimistic, pessimistic, and most likely scenarios for costs to account for uncertainty.

- It’s important to include a contingency reserve for unexpected expenses.

- Cost Budgeting:

- This process involves aggregating the estimated costs of individual activities or work packages to establish a total cost baseline for the project.

- The budget acts as a financial plan and a reference point against which actual costs will be measured.

- Cost Control:

- This is an ongoing process throughout the project lifecycle, involving monitoring actual expenditures against the approved budget and the cost baseline.

- Key activities include:

- Tracking and recording all project expenses.

- Identifying and analyzing cost variances (differences between planned and actual costs).

- Forecasting future costs based on current performance.

- Taking corrective actions to bring the project back on track if deviations occur (e.g., adjusting resource allocation, re-evaluating scope).

- Communicating financial status to stakeholders.

- Utilizing tools like Earned Value Management (EVM) to measure project performance in terms of cost and schedule.

Also See: Best Lean Six Sigma Training in Albuquerque

Final Words

Project cost management keeps spending on track. It protects project success. It involves planning, estimating, budgeting, and controlling.

Strong cost control saves money and avoids surprises. It also improves decision-making and boosts stakeholder confidence.

Every project needs careful cost management. Without it, even great ideas may fail. Start early, stay consistent, and learn from each project.

About Six Sigma Development Solutions, Inc.

Six Sigma Development Solutions, Inc. offers onsite, public, and virtual Lean Six Sigma certification training. We are an Accredited Training Organization by the IASSC (International Association of Six Sigma Certification). We offer Lean Six Sigma Green Belt, Black Belt, and Yellow Belt, as well as LEAN certifications.

Book a Call and Let us know how we can help meet your training needs.