First In, First Out (FIFO) is a critical principle in inventory management and accounting that ensures the orderly flow and valuation of goods within a business. It operates on the straightforward premise that the oldest inventory items (those received or produced first) are the first to be used or sold.

This method is not only fundamental for maintaining operational efficiency but also plays a crucial role in financial reporting and compliance.

Table of contents

Definition of FIFO

FIFO, abbreviated as “First In, First Out,” dictates that the first items received or produced are the first ones to be utilized or sold. This approach is particularly relevant in industries dealing with perishable goods or those facing risks of obsolescence, such as food, pharmaceuticals, and electronics.

Example

In a retail setting using FIFO, if a store receives three shipments of products at different costs over time—$10 per unit, $15 per unit, and $20 per unit—and subsequently sells a portion of these products, the store sells the $10 units first, as dictated by FIFO.

This method ensures that the costs associated with older inventory are recognized first, affecting how profits and taxes are calculated.

Principles and Operational Implementation

The core principle of FIFO revolves around maintaining the sequence of inventory as it enters and exits a company’s stock.

Implementing this involves using physical methods like designated storage lanes and digital systems that track the chronological order of inventory receipts.

By adhering to FIFO, businesses prioritize the sale or use of older inventory items before newer ones. This approach is particularly advantageous in industries dealing with perishable goods or products prone to technological obsolescence.

Difference Between FIFO and LIFO

| Basis | FIFO (First In, First Out) | LIFO (Last In, First Out) |

| Principle | Matches revenue with the oldest inventory costs. | Matches revenue with the newest inventory costs. |

| Inventory Valuation | The newest inventory items are sold or used first. | Matches revenue with newest inventory costs. |

| Cost of Goods Sold | Typically lower during inflationary periods. | Typically higher during inflationary periods. |

| Financial Reporting | Often results in higher reported profits. | Often results in lower reported profits. |

| Tax Implications | May have lower taxable income due to lower COGS. | May have higher taxable income due to higher COGS. |

| Risk Management | Reduces risk of obsolescence for older inventory. | Higher risk of obsolescence for older inventory. |

| Suitability | Suitable for industries with stable or declining prices. | Suitable for industries with rising prices. |

| Complexity | Generally simpler to administer and understand. | More complex due to valuation adjustments. |

| Regulatory Compliance | Complies well with IFRS (International Financial Reporting Standards). | Generally accepted under US GAAP (Generally Accepted Accounting Principles). |

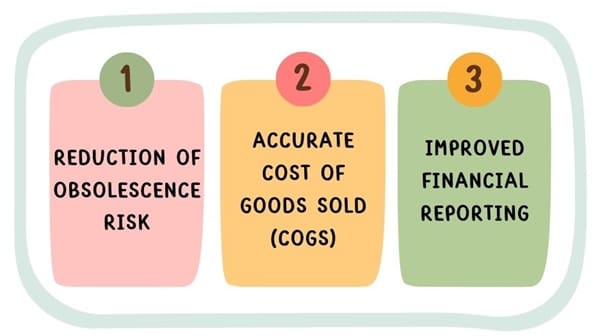

Advantages of FIFO

- Reduction of Obsolescence Risk: By selling older inventory first, FIFO helps mitigate the risk of inventory obsolescence. This is crucial for industries where products have limited shelf lives or where rapid technological advancements can quickly render goods outdated.

- Accurate Cost of Goods Sold (COGS): FIFO ensures that the cost associated with goods sold aligns with the oldest inventory costs. This results in a more accurate representation of profitability and financial health on income statements. In comparison, methods like LIFO (Last In, First Out) can distort profitability metrics during inflationary periods.

- Improved Financial Reporting: FIFO enhances compliance with accounting standards through its systematic approach to inventory valuation. This approach ensures adherence to accounting standards. It provides a clear audit trail and supports transparency in financial statements, helping businesses meet regulatory requirements and investor expectations.

Practical Applications

FIFO finds extensive application across various industries:

- Retail: It ensures that goods with earlier purchase dates are sold first, aligning with consumer expectations and regulatory requirements for perishable items.

- Manufacturing: It optimizes storage space and reduces holding costs. This is possible by ensuring that materials received first are used in production first, thereby helping manage raw material inventories.

- Pharmaceuticals and Food: Critical for industries where product safety and regulatory compliance demand adherence to expiration dates (FEFO—First Expire, First Out).

Financial Implications and Reporting

- Inventory Valuation: FIFO’s impact on inventory valuation is significant. By valuing inventory at older, potentially lower costs, businesses can avoid overestimating profits during periods of rising prices.

- Cost of Goods Sold: Calculation of COGS under FIFO involves matching revenue with corresponding older costs, offering a more accurate reflection of profitability compared to methods that prioritize recent acquisitions.

Final Words

First In, First Out (FIFO) stands as a robust and widely adopted inventory management and accounting method. Its ability to reduce obsolescence risk, enhance financial transparency, and comply with regulatory requirements makes it indispensable for modern businesses.

By prioritizing the use of older inventory items, FIFO not only optimizes operational efficiency but also ensures that businesses maintain accurate financial records and make informed strategic decisions based on reliable data. Understanding and effectively implementing FIFO principles are essential for businesses aiming to achieve sustainable growth and profitability in dynamic market environments.