Lean accounting represents a fundamental shift from conventional financial practices toward value-stream focused management. Unlike traditional cost accounting systems that emphasize detailed variance analysis and complex overhead allocations, lean accounting prioritizes simplicity, speed, and strategic decision-making.

This revolutionary approach emerged from the recognition that traditional cost accounting may be inappropriate today because modern businesses require real-time insights rather than historical cost breakdowns. Companies implementing lean manufacturing discovered their accounting systems created barriers rather than enabling continuous improvement.

The core philosophy centers on eliminating waste while providing meaningful financial information that supports operational decisions. Rather than tracking every penny through complex cost centers, lean accounting focuses on value streams – the complete flow of activities that deliver products or services to customers.

Table of contents

What Is Lean Accounting?

Lean accounting is a financial management system designed to support lean manufacturing and operational strategies. Rooted in the lean philosophy pioneered by Toyota, it focuses on eliminating waste, enhancing value, and providing real-time, actionable financial insights. Unlike traditional cost accounting, which often emphasizes labor and overhead allocations, lean accounting prioritizes simplicity, transparency, and alignment with customer value.

Imagine a factory floor buzzing with efficiency, where every process is optimized to deliver quality products with minimal waste. Lean accounting mirrors this by stripping away complex, time-consuming financial processes and replacing them with clear, value-focused metrics. It’s not just about crunching numbers—it’s about telling a story of how a business creates value for its customers.

Public, Onsite, Virtual, and Online Six Sigma Certification Training!

- We are accredited by the IASSC.

- Live Public Training at 52 Sites.

- Live Virtual Training.

- Onsite Training (at your organization).

- Interactive Online (self-paced) training,

Core Components and Framework

Lean accounting encompasses three primary elements that work synergistically to create an efficient financial management system. These components replace traditional departmental thinking with value-stream orientation.

Value Stream Costing forms the foundation by grouping all costs associated with specific product families or customer segments. Instead of allocating overhead through arbitrary drivers, this method tracks actual costs within each value stream, providing clearer visibility into profitability.

Performance Measurement shifts focus from traditional financial metrics toward operational indicators that drive improvement. Lean accounting emphasizes measures like first-pass yield, lead time reduction, and customer satisfaction rather than solely concentrating on cost variances.

Decision Support provides managers with timely, relevant information for strategic choices. The system eliminates complex calculations that delay decision-making, offering straightforward data that supports lean thinking principles.

These elements work together to create transparency throughout the organization while reducing administrative burden. Companies discover they can make better decisions faster when accounting systems align with operational realities.

Why Traditional Cost Accounting Falls Short?

Traditional cost accounting, while reliable for decades, often feels like a clunky relic in today’s dynamic markets. Here’s why it may be inappropriate today:

- Overemphasis on Overhead Allocation: Traditional systems allocate costs based on labor hours or machine time, which can distort the true cost of value-adding activities. This leads to inaccurate pricing and decision-making.

- Complexity and Waste: Detailed cost tracking creates mountains of data, much of it irrelevant to operational decisions. This wastes time and resources.

- Lag in Reporting: Traditional methods rely on month-end reports, which are often too late to influence real-time decisions.

- Misalignment with Lean Goals: Lean operations focus on flow and customer value, but traditional accounting often ignores these, focusing instead on inventory valuation and standard costs.

Lean accounting flips this script, offering a streamlined approach that aligns with modern business needs. By focusing on value streams rather than individual products or departments, it provides clarity and agility.

Core Lean Accounting Principles

To truly grasp lean accounting, let’s explore its foundational principles. These guideposts ensure financial practices support lean operations and drive continuous improvement.

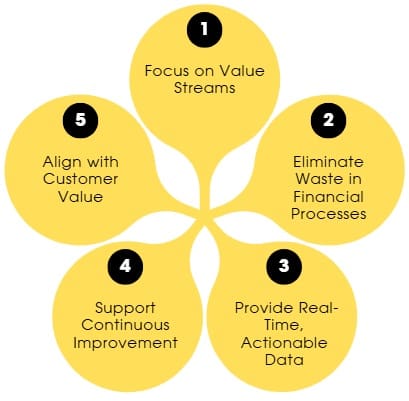

1. Focus on Value Streams

Lean accounting organizes financial data around value streams—the sequence of activities that deliver a product or service to the customer. Instead of tracking costs by department or product, lean accounting groups them by value stream, making it easier to see where value is created and where waste occurs. For example, a manufacturer might track the entire process of producing a widget, from raw materials to delivery, as a single value stream.

2. Eliminate Waste in Financial Processes

Just as lean manufacturing cuts non-value-adding activities, lean accounting eliminates unnecessary financial tasks. Complex variance reports, excessive budgeting details, and redundant data entry? Gone. Lean accounting replaces them with simple, visual tools like box scores, which provide a snapshot of performance metrics like revenue, costs, and productivity.

3. Provide Real-Time, Actionable Data

In a lean environment, decisions need to happen fast. Lean accounting delivers real-time financial insights through tools like value stream costing, which tracks costs as they occur. This empowers managers to make informed decisions on the spot, rather than waiting for month-end reports.

4. Support Continuous Improvement

Lean accounting isn’t static—it evolves with the business. By integrating with methodologies like Six Sigma accounting, it supports data-driven process improvements. Metrics like cycle time, defect rates, and customer satisfaction become part of the financial narrative, fostering a culture of continuous improvement.

5. Align with Customer Value

At its core, lean accounting ensures every financial decision reflects what customers value. By focusing on value streams and eliminating non-value-adding costs, businesses can price products competitively while maintaining profitability.

Also Read: Carbon Footprint

Lean Accounting vs. Traditional Cost Accounting

To understand the power of lean accounting, let’s compare it directly with traditional cost accounting:

| Aspect | Lean Accounting | Traditional Cost Accounting |

| Focus | Value streams and customer value | Individual products, departments |

| Cost Tracking | Simplified, real-time value stream costing | Complex, labor-intensive standard costing |

| Decision-Making | Real-time, actionable insights | Delayed, historical data |

| Waste | Eliminates non-value-adding financial tasks | Often generates excessive, irrelevant data |

| Alignment with Lean | Designed for lean operations | Often misaligned with lean principles |

This comparison highlights why lean accounting is a game-changer for businesses embracing lean methodologies. It’s not just a new way to count beans—it’s a strategic tool for driving efficiency and profitability.

Benefits of Lean Accounting

Adopting lean accounting offers a cascade of benefits that ripple across the organization:

- Improved Decision-Making: Real-time data empowers managers to act swiftly, whether adjusting production schedules or optimizing pricing.

- Reduced Costs: By eliminating wasteful financial processes, businesses save time and resources.

- Enhanced Transparency: Simple metrics like box scores make financial performance clear to everyone, from shop floor workers to executives.

- Better Customer Value: Aligning costs with value streams ensures businesses focus on what customers truly want.

- Support for Lean Culture: Lean accounting reinforces a culture of continuous improvement, aligning financial goals with operational ones.

For example, a mid-sized manufacturer adopting lean accounting might reduce its budgeting cycle from weeks to days, freeing up staff to focus on strategic initiatives. Meanwhile, real-time cost data could help identify a bottleneck in production, saving thousands in wasted resources.

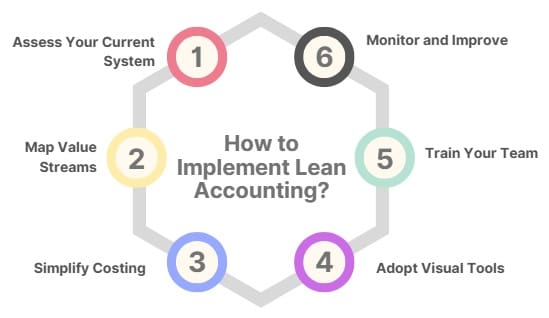

How to Implement Lean Accounting?

Ready to embrace lean accounting? Here’s a practical roadmap to get started:

Step 1: Assess Your Current System

Evaluate your existing accounting practices. Are they aligned with lean principles? Identify areas of waste, such as excessive reporting or complex cost allocations.

Step 2: Map Value Streams

Identify your business’s value streams. For a manufacturer, this might be the process of producing a specific product line. For a service company, it could be the delivery of a key service. Map these streams to understand where value is created.

Step 3: Simplify Costing

Shift from traditional standard costing to value stream costing. Track costs at the value stream level, focusing on direct costs like materials and labor directly tied to customer value.

Step 4: Adopt Visual Tools

Implement tools like box scores or lean performance dashboards. These provide a quick, visual overview of financial and operational metrics, making it easy to spot trends and issues.

Step 5: Train Your Team

Lean accounting requires a cultural shift. Train employees at all levels to understand value streams, interpret lean metrics, and use financial data to drive improvements.

Step 6: Monitor and Improve

Lean accounting is about continuous improvement. Regularly review your processes, gather feedback, and refine your approach to stay aligned with business goals.

Also Read: Makigami

Common Misconceptions About Lean Accounting

Let’s debunk some myths to clarify what lean accounting is not:

- Myth 1: Lean Accounting Is Just Cost-Cutting

While it reduces waste, lean accounting is about aligning financial practices with value creation, not just slashing budgets. - Myth 2: It’s Only for Manufacturing

Lean accounting applies to any industry, from healthcare to software development, where value streams and efficiency matter. - Myth 3: It Replaces All Traditional Accounting

Lean accounting complements traditional methods, focusing on operational efficiency while still meeting regulatory requirements.

Lean Accounting and Six Sigma

Lean accounting pairs beautifully with Six Sigma accounting, which uses statistical methods to reduce variability and improve quality. Together, they create a powerful framework for operational and financial excellence.

For instance, Six Sigma’s focus on defect reduction can inform lean accounting’s value stream analysis, ensuring costs are tied to high-quality outputs. This synergy drives both efficiency and customer satisfaction.

Challenges of Adopting Lean Accounting

No transformation is without hurdles. Common challenges include:

- Resistance to Change: Employees accustomed to traditional accounting may resist new methods.

- Initial Investment: Training and system changes require upfront time and resources.

- Data Integration: Shifting to real-time data may require new software or processes.

However, these challenges are outweighed by long-term gains in efficiency, clarity, and profitability.

FAQs About Lean Accounting

What is lean accounting?

Lean accounting is a financial management approach that aligns with lean principles, focusing on value streams, waste elimination, and real-time data to support efficient operations.

How does lean accounting differ from traditional cost accounting?

Lean accounting emphasizes value stream costing, real-time insights, and simplicity, while traditional cost accounting focuses on complex allocations, historical data, and department-based tracking.

Which are correct statements about lean accounting?

- It supports lean operations by focusing on value streams.

- It eliminates wasteful financial processes.

- It provides real-time, actionable data.

- It’s only for manufacturing (incorrect—lean accounting applies to all industries).

Can lean accounting work with Six Sigma?

Yes, lean accounting complements Six Sigma by aligning financial metrics with quality improvements, creating a holistic approach to efficiency and profitability.

Why is traditional cost accounting inappropriate today?

Traditional cost accounting often relies on outdated methods like complex overhead allocations and delayed reporting, which misalign with modern lean operations and real-time decision-making needs.

Final Words

Lean accounting is more than a buzzword—it’s a strategic shift that aligns financial management with the demands of today’s lean-driven businesses. By focusing on value streams, eliminating waste, and delivering real-time insights, it empowers organizations to make smarter decisions and deliver greater customer value.